Don’t risk making your business exit without an exit strategy

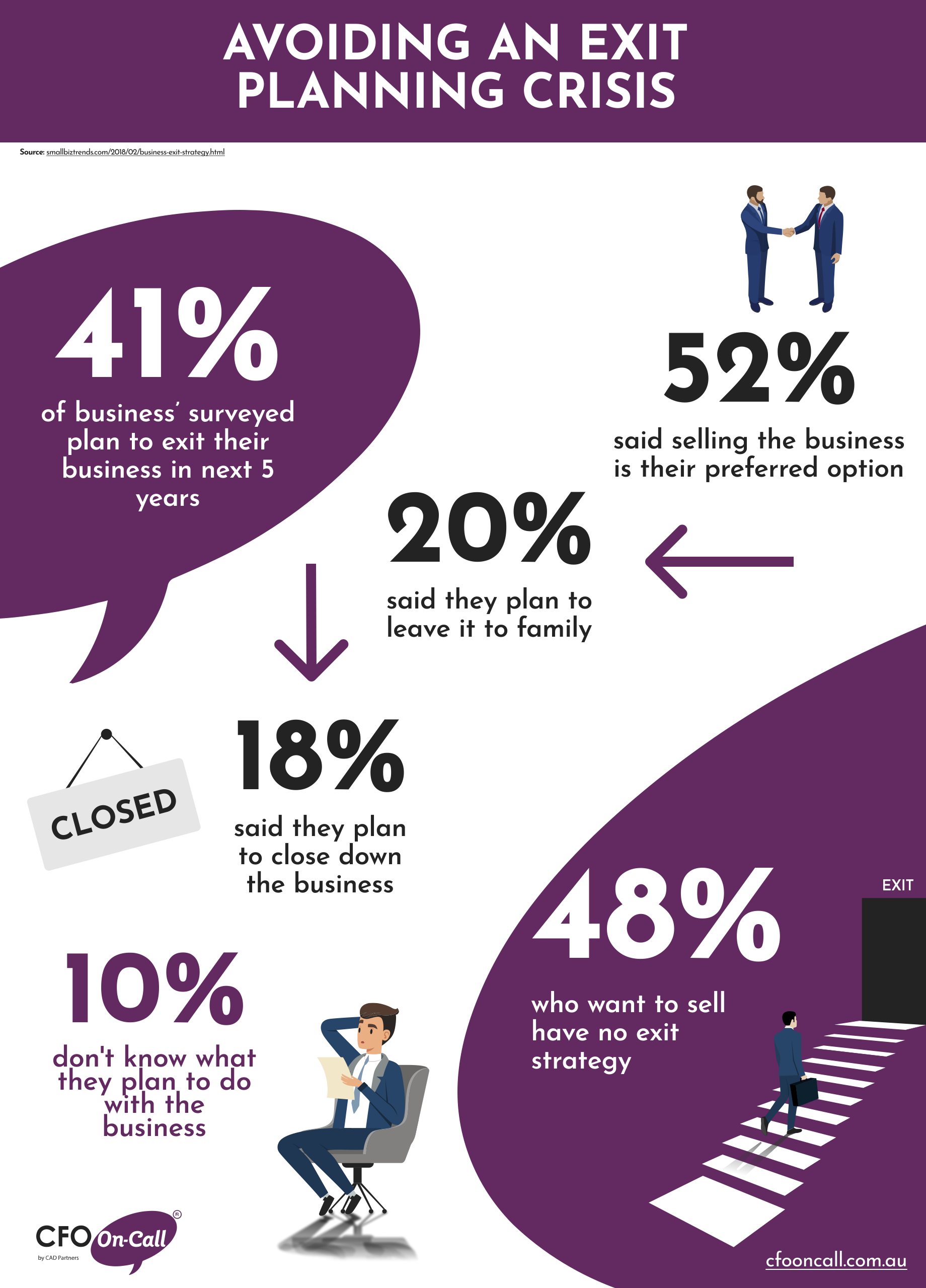

If you’re like most business owners, you have plans to one day retire, leaving a healthy legacy for others to carry on into the future, and reap the rewards of your years of hard work. The trouble is, according to a Voice of Australia Business Survey, only 19% of small to medium enterprise owners in Australia have a succession or retirement plan,

The majority of business exits occur upon sale of the business, but selling a business isn’t a simple proposition like selling a car, or any other piece of equipment. It’s far more complicated, with multiple factors impacting its value, including customers, suppliers, staff & management – but it can also be far more valuable, as long as you know how to sell it.

In this article, we’ll cover factors to consider when you want to maximise the exit value of your business.

Topics of discussion:

What is an exit strategy plan?

An exit strategy plan is a plan for how you will eventually leave your business. This plan will typically include one of several options; for example, mergers, acquisitions, IPOs, and exits by liquidation. The idea of the exit strategy plan is to cover all the key considerations for potential investors so that you can sell the business at a high price point.

Why is it important to have an exit strategy?

The need for an exit strategy isn’t only for owners who are planning on leaving their businesses – it’s for all business owners who want a flexible blueprint and measurement strategy for success. Your exit strategy can guide you through changing circumstances and towards the goal you want to achieve, namely exiting the business with a substantial profit to your name and leaving a legacy that carries on.

When should you begin to plan your business exit?

If your business is also your retirement fund, you may need to start thinking about selling quite a while before your actual sale day. In some cases, the best time to start planning may be a number of years beforehand – and in any case, the best time to start planning is now.

According to Sue Hirst from CFO On Call, there is no such thing as “too early” when it comes to planning your business exit. “Business owners are so caught up in the day to day management of the business that there is a tendency to prioritise matters that are urgent over matters that are important,” Sue said. “Sometimes, things can happen unexpectedly – people become disabled; people die. Even if your business is in growth mode and you have no thoughts of retirement, you still need to deal with the contingencies of a forced exit.”

Why should you plan early for your business exit?

A sale like this takes a lot of planning, and that’s not easy when you’re caught up in the daily business functions. Planning early gives you the best possible chance to grow the value of your business and make it attractive to potential buyers. This is especially important if you have been central to the business for a long time, because you’ll need to create systems that allow the business to function effectively without you. It takes time to implement these changes and see results.

Questions to ask about your exit strategy

What are industry trends indicating?

Most people want to buy a business of ‘today and tomorrow’, not ‘yesterday’ – a business that keeps up with current trends – so you need to take these into consideration and be realistic about the value, taking into consideration current trends.

Key questions include:

- Is your business in a well established, growing and stable industry?

- Can it be negatively impacted by industry restructuring or negative global trends?

- Will future industry trends positively affect the business?

How do you measure business performance?

The most common measures of business performance are profit and cash flow. In the past, some businesses were run based on tax minimisation – but now it’s time to switch into a ‘profit maximisation’ mindset. If the business is struggling with profit and cash flow, it won’t be as attractive to a potential purchaser. They may even expect a discount for poor results – but by some forethought and focus on profit maximisation, you can eliminate the risk of this happening.

Key questions include:

- How many years of profitable trading does your business have?

- Have you experienced sales and gross margin increase or decrease in the current year?

- Has your wages bill increased as a percentage of sales?

- Is there an improvement in liquidity (debtors collection, stock turnover, etc.) and is the business able to control or reduce operating expenses?

What is important for business growth?

A potential purchaser will want to leverage the opportunities for growth that currently exist in your business – and the fewer there are, the bigger discount they will want. To answer this question, you’ll need to look at both past and future performance predictors.

Key questions include:

- Do opportunities for business growth exist e.g. can the current market be worked harder, can new products/services be introduced or new geographical areas opened up?

- If so can they be practically pursued?

- Has there been a history in the business of continual research and development and is plant and equipment in good order?

- Are the current premises able to support growth?

- Is there a formal business plan in place (including SWOT, Growth, Budgets, Cost Centre Analysis, Strategic Plan, Marketing Plan, etc.)?

What are the main risks to the business?

The riskier the business opportunity, the less attractive (and hence valuable) it is to a purchaser. Top risks in your business fall under several major categories, including economic trends, legislation, insurance options, and technological developments.

Key questions include:

- Is the cost of your supplies subject to inflationary pressures and/or exchange rate/fuel prices?

- Are your customers in depressed geographical regions?

- Does government legislation protect the supplies you make and are they threatened by imports?

- Is there adequate insurance in place e.g. Work Cover, Professional Indemnity, or General Insurance?

- Are your products/services threatened by new technology, IT or the web? If so, have you done anything about it and adjusted your business model?

- Have you had any legal claims in the recent past?

- Is the location of your premises important, and if so, is tenure secured?

- Has your business recently been affected by disruptions to input supply? If so, what is your plan to deal with this?

- How large is your pool of suppliers, and how reliant are you on the suppliers you currently use to dictate the products or services you offer?

What are the barriers to entry in your market?

In most industries, business owners should expect to come up against a handful of competitors, but too many (or too few) could be a red flag. The main problem with an undersaturated market is that it may encourage your potential successors to start their own business in competition instead of taking over yours.

Key questions to ask yourself about your competitors include:

- Are they aggressive and is there increased competition from national and overseas competitors?

- Can the market sustain the current level of competition?

- Is there a high cost or skills/knowledge barrier to start up?

- Could new competitors have access to greater resources than you?

What Management Information Systems do you use?

A purchaser will want to be very clear about the accuracy of the results of the business, and that relies on your ability to manage information effectively.

Key questions here include:

- Do you operate computerised accounting and a management reporting system?

- Do you report on sales, cost of goods sold, employee and profit by major products/services categories?

- Do you have regular monthly reporting in place?

- Do you follow best practice operating systems?

How can you reduce owner reliance?

Developing a management team around you is a start; however, ensuring this is sustainable takes time to implement, so start early. Minimising reliance on the business owner or manager is important to maximising the value of the business.

Key questions here include:

- How reliant is the business on the current owner?

- Will the knowledge be easy to transfer?

- Will the departure of the current owner cause loss of key customers and staff?

Loyal customers keep businesses thriving (Source: https://unsplash.com/photos/q3o_8MteFM0)

Customers and staff are a great asset of any business, so anything you can do to secure them is important. Purchasers want to be confident about the future viability of the business they are entering into, and that means having people to sell to.

Key questions here include:

- How loyal are the customers who make up the top ten percent of your sales?

- What percentage of your customers are responsible for generating 80 per cent of your profits?

- How strong is the demand for your products/services, and do substitutes exist?

- Would it still be strong if your prices were to increase by 10 per cent?

What is your staff turnover?

Staff are an important asset of any business – so much so that staff turnover is a major Human Resources KPI, and may be a major red flag for a potential buyer. Anything you can do to secure your staff members could potentially increase business value. If you’re unsure about your staff members’ commitment to the organisation goals and visions, consider a formal staff appraisal.

- Is the industry losing staff to other industries? To put it in context, think of mining – when the boom is on, tradespeople flock to where the money is and builders find it very hard to get good staff.

- How experienced and knowledgeable are your key staff?

- What is your staff retention history, and do you have strategies for staff recruitment, retention and motivation?

- Is there good communication with staff?

What is your succession and estate planning process?

If you think of your business like a house, the exit strategy plan is an opportunity to renovate before you sell and get the best possible price.

Because you know the business and the industry better than anyone, you are in a great position to perform the renovation, and if you’re willing to stay in and do the work, you stand to make a premium profit a few years from now. In any case, now is the time to start planning.

Key questions here include:

- Do you have risk insurance in place (Life, TPD, Key Person etc.) for owners and relationship partners?

- Is there a documented business life plan, succession plan and estate plan?

- Is there capital for future growth and succession and strategies in place to protect, grow and realise optimal business value?

- In essence, is the business easy to sell?

Realistically, most Business Owners are so focused on creating, building and managing their businesses that they don’t have much time to plan an exit from the business – but don’t despair! You don’t have to do all the work yourself. We have experienced advisors across Australia and New Zealand to help guide you through the process.

Ready to book a call with a CFO? Contact us today on 1300 36 24 36 for an obligation-free chat!